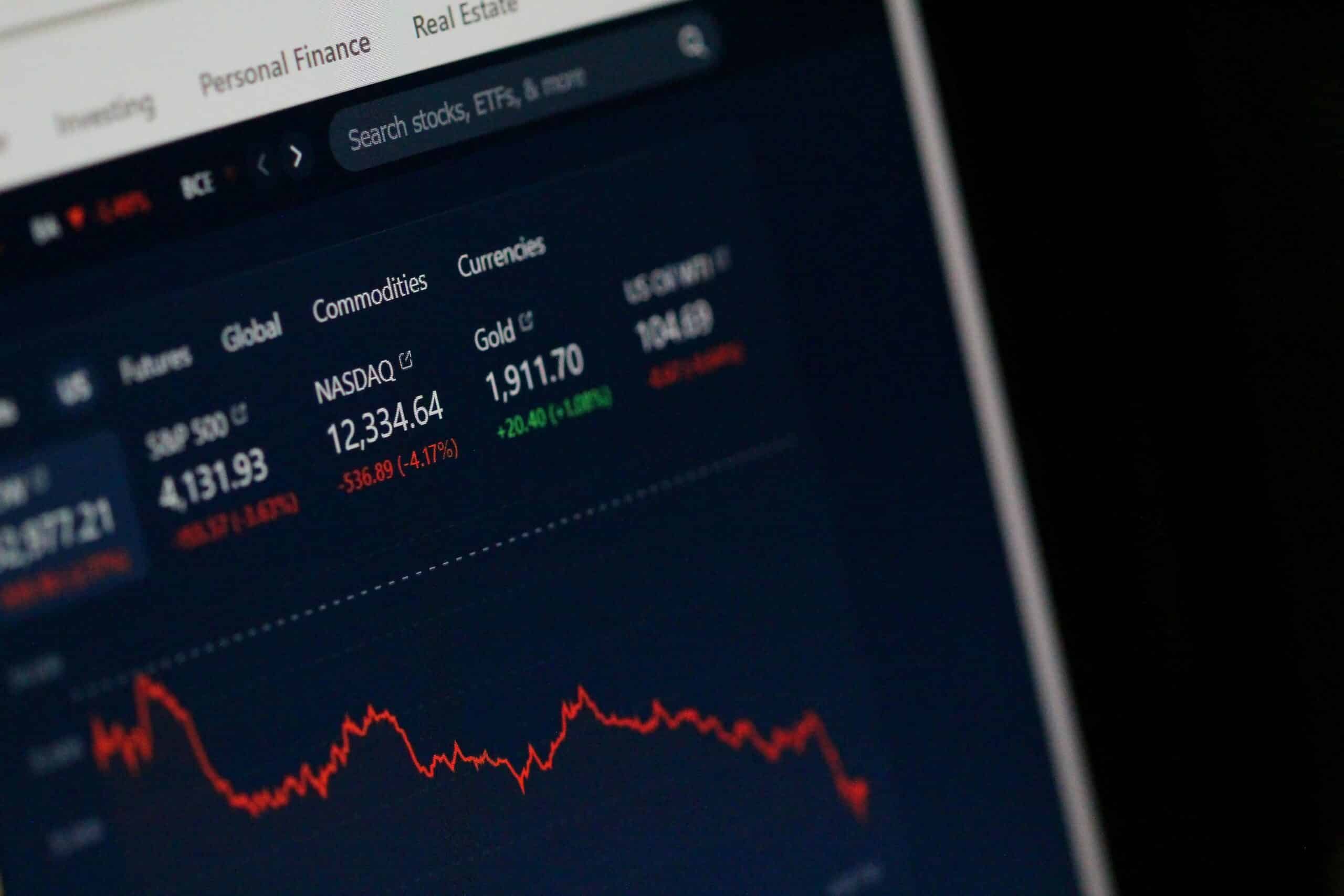

This quarter was dominated again by yields, but the unexpected player of the quarter was oil, up by nearly 30% in the quarter – the mix between these two forces lead all major indexes lower for Q3.

Rates: The fed is firmly in charge, and the narrative of “higher for longer” is now firmly in place. Longer-dated USD rates are now at 15-year highs, and the market is now expecting it to stay up there.

Oil: Saudi and Russia led the way in Q3 with continued production cuts.

Index returns for the quarter: S&P (-3.65%), Nasdaq (-4.12%), Eurostoxx (-8%), Nikkei (-7.3%), Hang Seng (-5.8%), Alsi (-5.26%)

The mighty RAND (ZAR) was almost flat in the quarter, starting at 18.84 and finishing at 18.92, but with an impressive 10% range of 17.27 -> 19.33

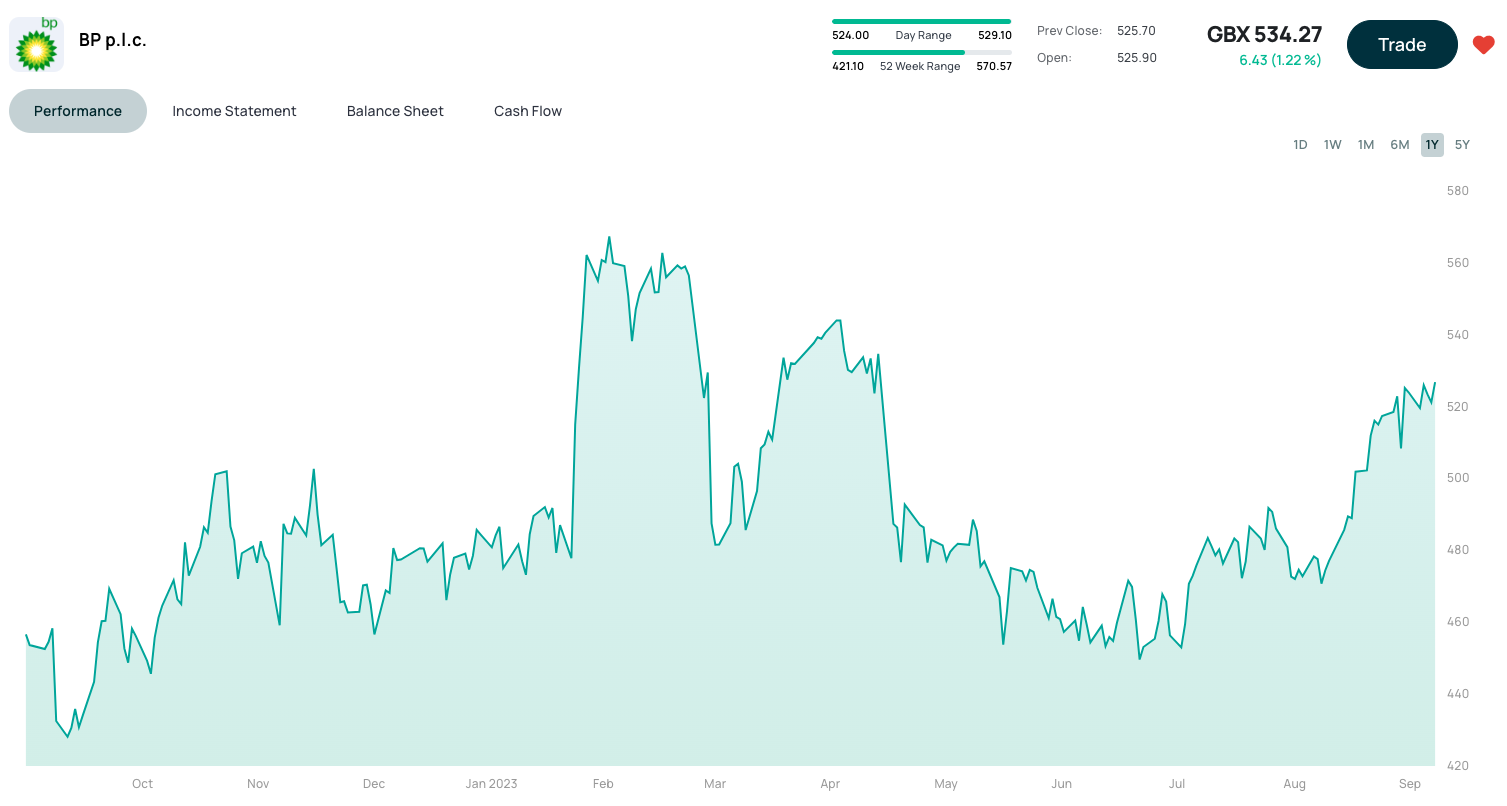

It is always good to stand still and reflect on what drove the markets for the last three months, before we look toward Q4.. On the back of strong OIL, energy stocks got a leg up across all markets, with banks also enjoying solid returns in this higher rate environment before we see meaningful credit losses coming through, where these higher rates will start hurting the consumer.

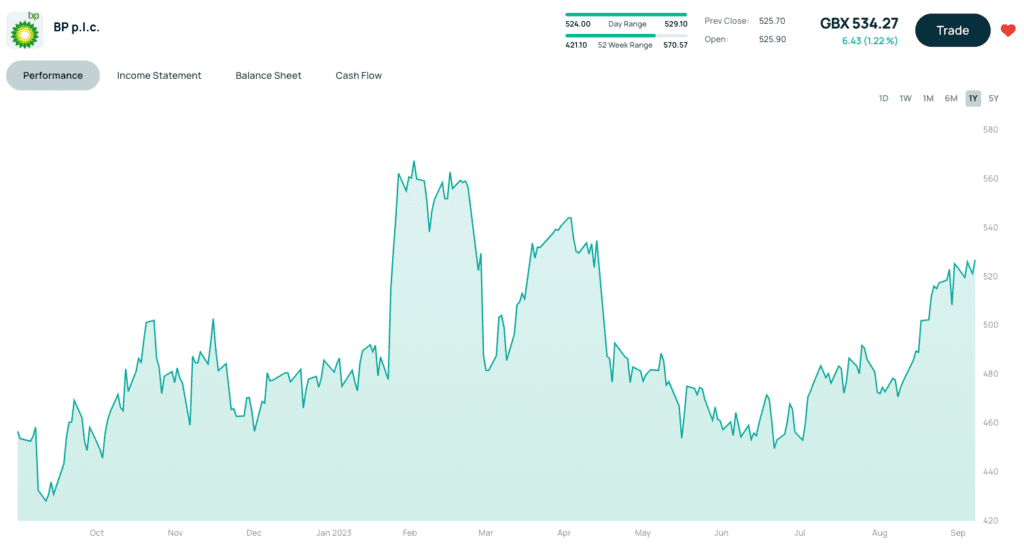

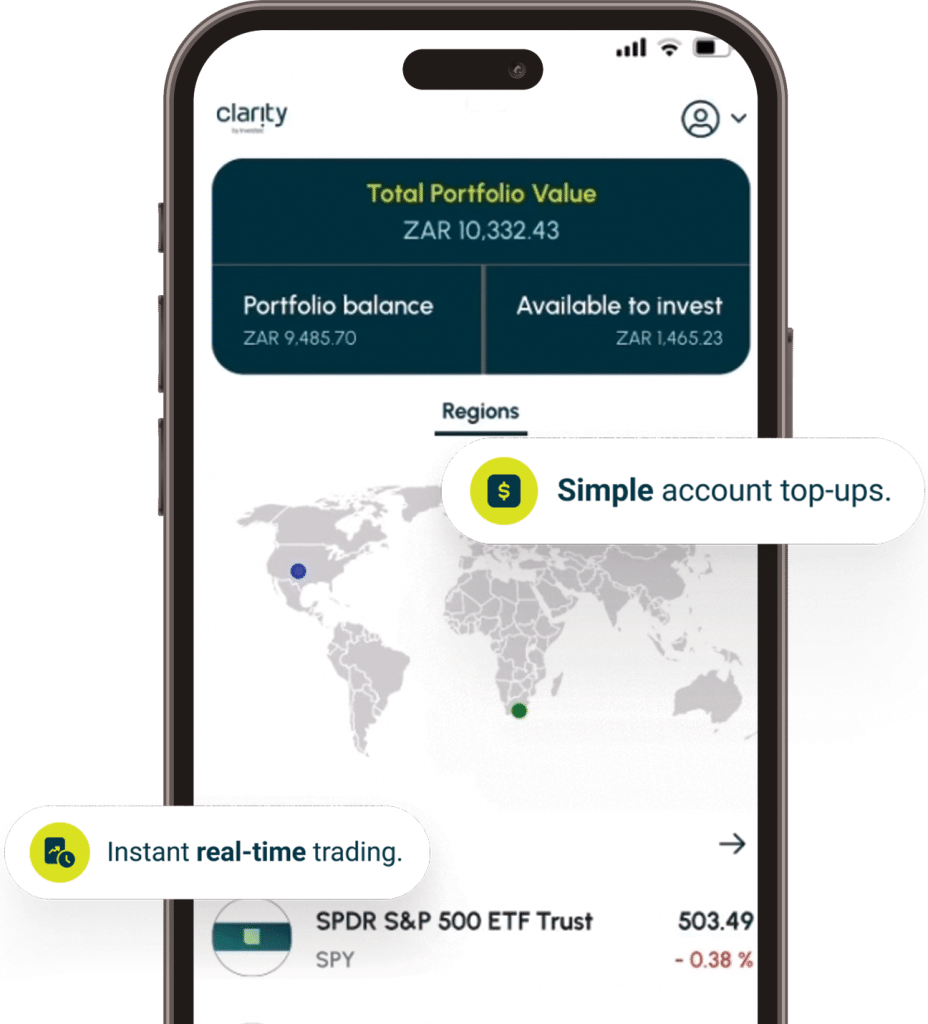

ZAR -> USD -> BP in under 2 minutes on Clarity.