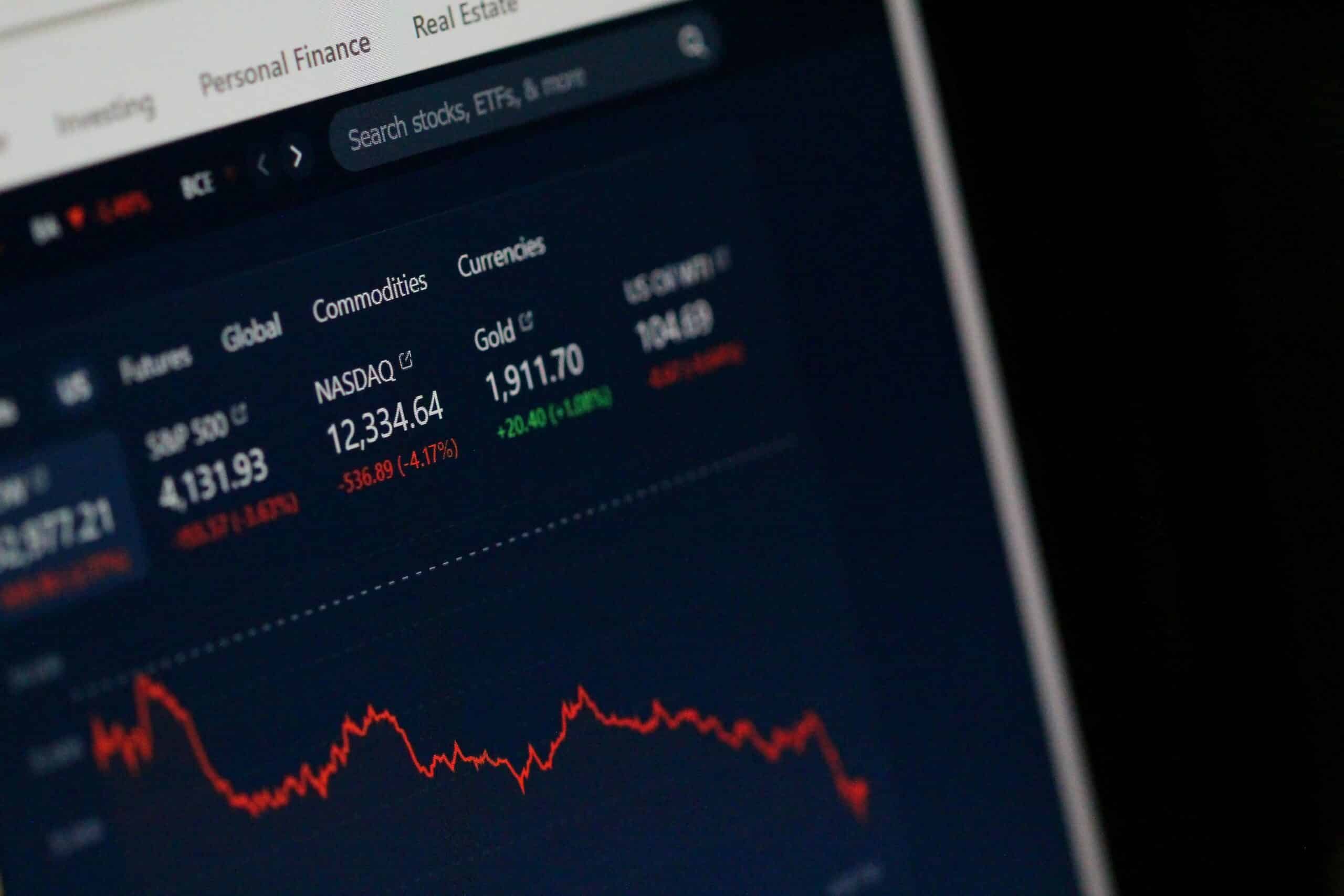

Tech stocks remain the major drivers behind the multiple record highs achieved on the S&P 500 (VOO-NASQ) and Nasdaq 100 in 2024.

Artificial intelligence (AI) as a strong thematic investment trend that still has lots of room to run, but the story behind the tech market rise is more nuanced, with semiconductor stocks the true out-performers among sector stocks.

The semiconductor industry is the backbone of all modern technology, with the technology considered one of the most transformative inventions in history, holding applications across multiple industry verticals, including cloud computing, automotive, computation and data storage, wireless technology and AI.

Little wonder then that semiconductor stocks have advanced at breakneck speed in 2024. The Semiconductor Industry Association (SIA) announced global semiconductor industry sales totalled $149.9 billion during the second quarter of 2024, an increase of 18.3% compared to the second quarter of 2023 and 6.5% more than the first quarter of 2024.

While a largely cyclical sector, modern society’s unrelenting march towards ubiquitous computing, AI-infused everything, and all forms of automation, from self-driving cars to robotics, have made these chips indispensable.

Given the relevance and reliance on semiconductors in just about every sphere of technological advancement, McKinsey & Company predicts that the global industry is “poised for a decade of growth and is projected to become a trillion-dollar industry by 2030”.

A McKinsey analysis based on a range of macroeconomic assumptions suggests the industry’s aggregate annual growth could average 6-8% a year up to 2030, which would make it a $1 trillion industry by the end of the decade, with three sectors: automotive, computation and data storage, and wireless, predicted to drive about 70% of this growth.

The rise of data centres and cloud computing has driven demand for semiconductors as these facilities rely on vast numbers of servers, each containing multiple processors and memory chips.

The proliferation of Internet of Things (IoT) devices, from smart homes to industrial automation, has also created a need for smaller, more energy-efficient semiconductors, which has led to innovations in microcontrollers and system-on-chips (SoCs).

In addition, the rollout of 5G networks and the development of 6G technologies require advanced semiconductors to handle the increased data traffic and speed, fuelling demand for radio frequency (RF) chips and other specialised components.

AI is the other major semiconductor driver, with the biggest chip maker by market cap, Nvidia (NVDA-NASQ), estimating that total demand for the graphics processing units (GPUs) needed to support AI systems could reach $2 trillion, with $1 trillion from data centres and $1 trillion from work connected to AI, such as training new large language models (LLMs), machine learning and scientific simulations.

The Deloitte 2024 Semiconductor Industry Outlook adds that generative AI (GenAI), is the major driver behind sales in 2024, as the market for chips that accelerate the training and inference of generative AI models, especially deep learning models, spurs demand due to the immense computational power required by these technologies.

Rising demand is prompting new industry investments to increase chip production, with the landmark CHIPS and Science Act in the United States (US) a key piece of legislation aimed at securing the country’s position as the market leader in global AI and technological advancement.

Following the Act’s implementation, data from the SIA State of the Industry Report shows that companies in the semiconductor ecosystem had announced more than 90 new manufacturing projects in the US, totalling nearly $450 billion in announced investments across 28 states, with additional investments planned in countries around the world to create a more resilient supply chain.

According to a 2024 SIA-Boston Consulting Group report, in the decade following CHIPS enactment (2022 to 2032), the US is projected to more than triple its semiconductor manufacturing capacity — the highest rate of growth in the world during that period.

The report also forecasts the US will grow its share of advanced (less than 10nm) chip manufacturing to 28% of global capacity by 2032 and capture 28% of total global capital expenditures (capex) from 2024 to 2032.

The semiconductor industry includes a host of high-revenue earning, high-growth companies that produce a wide range of semiconductors, making them ideal companies to include in a portfolio.

These companies compete to produce smaller, cheaper, and faster chips for increasingly powerful and affordable technology products across four main product categories:

- Microprocessors;

- Memory chips;

- Commodity integrated circuits, and;

- Complex systems on a chip (SoCs)

The major global semiconductor companies include players from the US, South Korea, and the Netherlands, such as Nvidia (NVDA-NASQ), Broadcom (AVGO-NASQ), Super Micro Computer Inc. (SMCI-NASQ), Micron Technology Inc. (MU-NASQ), Advanced Micro Devices (AMD-NASQ), Intel (INTC-NASQ) and Qualcomm (QCOM-NASQ).

Despite the cyclical nature of the industry, the bottom line is that semiconductors have rapidly emerged as the foundation of the modern tech industry.

Their performance and availability directly impact the capabilities of AI systems, data centres, IoT devices, and communication networks. As these technologies continue to evolve, the demand for semiconductors will likely remain strong, driving the growth of semiconductor companies and the broader tech sector.